Your credit score is a three-digit number that reflects your creditworthiness. It is an essential factor in determining your loan options, interest rates, and terms. When you apply for a loan, lenders will review your credit score to assess the risk of lending you money. The higher your credit score, the better your loan options and interest rates will be. In this blog, we’ll take a closer look at how your credit score affects your loan options and what you can do to improve it.

Understanding Your Credit Score

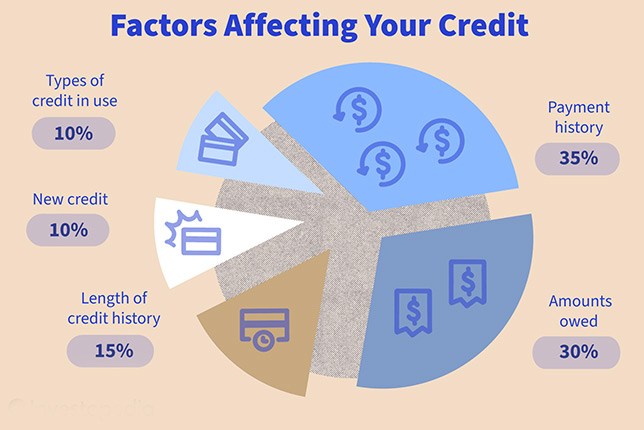

Your credit score is calculated based on several factors, including your payment history, credit utilization, length of credit history, new credit accounts, and credit mix. The most commonly used credit score model is the FICO Score, which ranges from 300 to 850. Here’s a breakdown of the FICO Score ranges:

- Excellent credit: 800 and above

- Very good credit: 740-799

- Good credit: 670-739

- Fair credit: 580-669

- Poor credit: 579 and below

Lenders use credit scores to evaluate the risk of lending money to a borrower. A high credit score indicates that you’re responsible with credit and can be trusted to repay the loan. A low credit score suggests that you may be a high-risk borrower and may have trouble repaying the loan. As a result, lenders are likely to charge you higher interest rates and may offer you less favorable loan terms.

How Credit Scores Affect Loan Options

Credit scores have a significant impact on the types of loans you can get and the interest rates you’ll pay. Here are some of the most common loan types and how credit scores affect them:

Mortgage Loans

Mortgage loans are used to finance the purchase of a home. They are typically long-term loans, with repayment periods of 15 to 30 years. When you apply for a mortgage loan, lenders will review your credit score to determine your eligibility and interest rate.

If you have an excellent credit score (800 or above), you’re likely to get the best interest rates and terms. On the other hand, if you have a poor credit score (below 580), you may not qualify for a mortgage loan at all. If you do qualify, you may have to pay higher interest rates and fees, which can add up to thousands of dollars over the life of the loan.

Auto Loans

Auto loans are used to finance the purchase of a car. Like mortgage loans, they are long-term loans with repayment periods of three to seven years. When you apply for an auto loan, lenders will review your credit score to determine your eligibility and interest rate.

If you have an excellent credit score, you’re likely to get the best interest rates and terms. On the other hand, if you have a poor credit score, you may not qualify for an auto loan at all. If you do qualify, you may have to pay higher interest rates and fees, which can add up to thousands of dollars over the life of the loan.

Personal Loans

Personal loans are unsecured loans that can be used for a variety of purposes, such as consolidating debt, financing a home renovation, or paying for unexpected expenses. Unlike mortgage and auto loans, personal loans have shorter repayment periods, usually between one and seven years. When you apply for a personal loan, lenders will review your credit score to determine your eligibility and interest rate.

If you have an excellent credit score, you’re likely to get the best interest rates and terms. On the other hand, if you have a poor credit score, you may not qualify for a personal loan at all. If you do qualify, you